New para-xylene capacity in China and also in the Middle East and the rationalization of uncompetitive production in the US and Western Europe have massively changed global trade flows.

Para-xylene (PX) is an important chemical intermediate, used primarily as a feedstock for polyester, purified terephthalic acid (PTA), and polyethylene terephthalate (PET).

PX global trade volume peaked in 2018 at 22.5 million tons after steadily increasing since 2010, but has since fallen below 2014 levels, to 15.0 million tons in 2023 (projected).

Intra-regional trade within Asia-Pacific consistently accounts for 70-80% of that trade.

Chinese imports of PX clearly underpin the regional and global trade dynamics, with China’s movement towards PX self-sufficiency heavily influencing the decline in global trade volume. In 2023, at 9.1 million tons of imports, China still dwarfed the next largest importing countries, which included Taiwan (1.3 Mt), the United States (1.2 Mt), India, and Mexico. It is worth noting that US imports have increased by nearly 350% over the past decade (from 270 Kt).

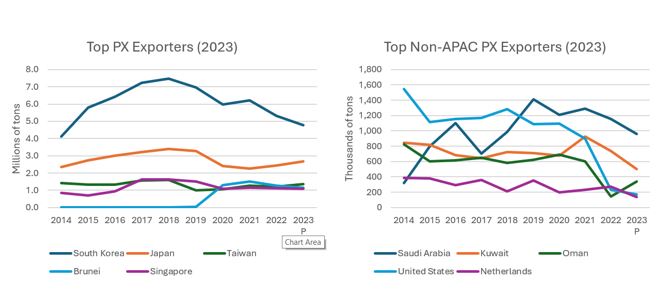

The five most significant exporters of PX globally in 2023 – South Korea (4.8 Mt), Japan (2.7 Mt), Taiwan (1.3 Mt), Brunei, and Singapore – also represent the top five suppliers to China.

Outside of Asia-Pacific, the Middle East remains the top net exporting region, led by Saudi Arabia (958 Kt in 2023), Kuwait (499 Kt), and Oman. US exports of PX have fallen precipitously since 2014, from 1.5 Mt to 232 Kt.

From International Trader Publications P-Xylene World Trade Analysis, a continuously updated online analysis of global trade developed from the latest statistics from all available countries.